Gold Hits $3,000: Pros, Cons and Outlook for 2025

During the 1896 US presidential election, William McKinley supporters took to wearing gold lapel pins, neckties, and headbands. McKinley’s supporters were demonstrating their support for gold against the “silver menace”. Keen to protect the gold standard, the McKinley campaign was successful in rejecting a bimetallic standard. The term “gold bug” originated as a label for those who favoured basing the U.S. monetary system on gold to the exclusion of silver. The definition has since expanded and is now applicable to individuals who are bullish on gold. Gold bugs are particularly excitable at the moment. Gold hit a record $3,004.86 per ounce on Friday. With prices having risen by 14% since the start of 2025, how justified is their enthusiasm?

2025 – an all-time high

The yellow metal has seen many periods of rapid price increase and subsequent corrections following what many subsequently judged to be an asset price bubble. Gold bugs argue that as fiat currencies decline in value (through inflation and rising national debt), refuge and return should be sought in the precious metal given it has a finite supply and, therefore, a long term store of value.

The policies of the Trump administration are making financial markets particularly volatile in 2025. This volatility is only adding to the appeal of safe haven assets like gold. The escalating trade war between the US and some of its largest trading partners has unsettled markets. The concerns around tariffs on US gold imports have triggered panic buying along with a rotation out of richly priced US equities into short dated treasuries and gold. In February, vast quantities of physical gold were purchased in London and shipped to New York in a move aimed at avoiding a potential tariff on gold imports into the US. There was also a concern that the Trump administration might revalue the gold held by the U.S. Treasury to market prices (from $42 / oz), increasing its value by c. $800 billion. The idea was that this gold could then be leased to the Federal Reserve, boosting liquidity in the markets and driving up gold prices. However, the US Treasury Secretary, Scott Bessent, has since dismissed this plan.

The current position is further being driven by conflicts and tensions in both Russia/Ukraine and the Middle East. Uncertainty is high and seems to be rising almost by the day. Meanwhile, central banks have also been buying up gold, especially in countries like Russia and China. The metal is finding growing applications in diverse fields such as nanotechnology, artificial intelligence (AI), cancer therapy, and malaria treatment. With this backdrop, 2025 has so far mustered the perfect storm resulting in gold breaking through the psychological $3,000 barrier.

The case for gold

For millennia, gold has been revered as a symbol of beauty, a form of currency, a valuable commodity, and at times, a useful investment. In more recent times, gold investing has become easier to access through a range of retail products such as Exchange Traded Contracts, making it an appealing addition to some client portfolios:

- Portfolio Diversification: gold has a low correlation to other asset classes. It can provide diversification benefits and potentially improve the risk-return characteristics of investor portfolios.

- Wealth Preservation: one of the main attractions is that it can be an excellent ‘store of value’. This was seen in the wake of the 2008 Global Financial Crisis and the COVID-19 pandemic. In these crises, investors turned to gold to hedge themselves against currency devaluation and preserve their purchasing power.

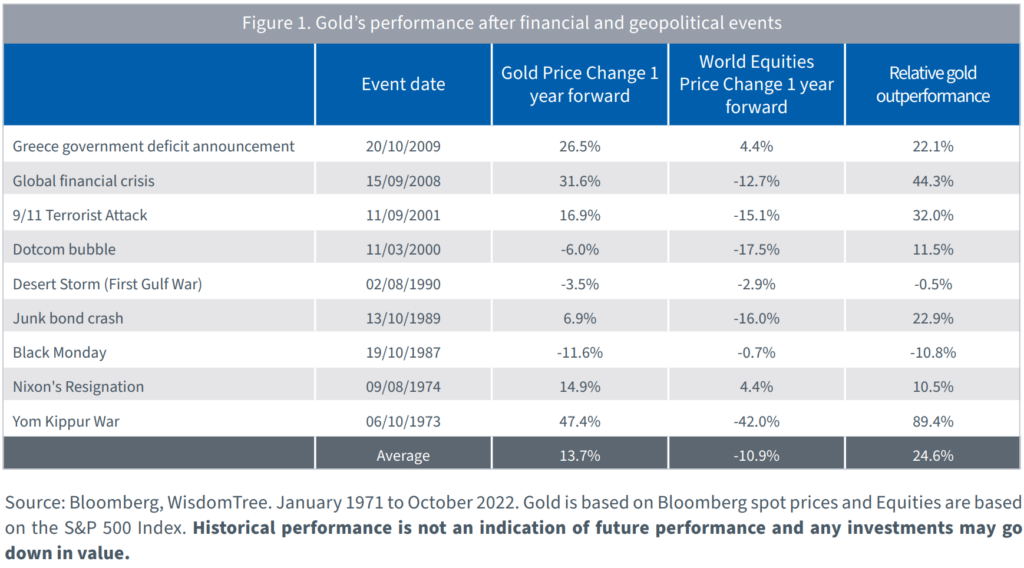

- Hedge Against Geopolitical Risk: when the Geopolitical Risk Index (GPR) has risen 2 standard deviations above its historic average, gold has risen 6.1% on average, while the S&P 500 Equity Index has fallen 7.4% in those months.

- Investor Psychology: rightly or wrongly, people trust it. To John Pierpoint Morgan (founder of JP Morgan): ‘Gold is money. Everything else is credit.’ Whilst things were a little different back in the late 1800s, it’s fair to say that many still regard gold as universally acceptable as a medium of exchange.

Drawbacks

Like all asset classes, there are limitations which investors must consider:

- No cash flows: as a non-income-producing asset, it does not offer an earnings or dividends stream. To profit from gold, its price must increase.

- Volatility: gold can be volatile. It makes a great diversifier to a portfolio because it behaves differently, not because it has a low volatility. In some years it has posted close to 30% losses (2013).

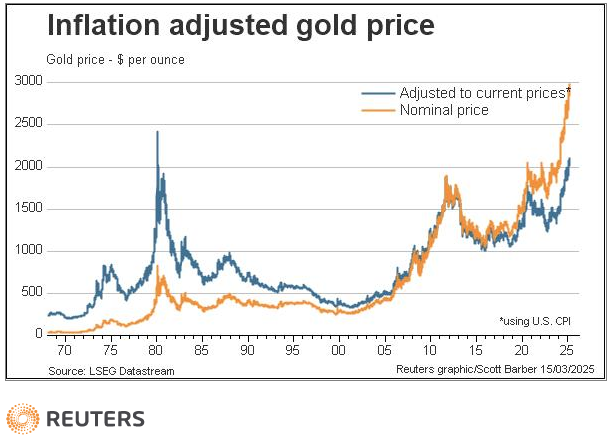

- Inflation Hedge: popular belief touts gold as a hedge against inflation. But how true is this over the long term? Take the gold price at the end of 2024 – $2,625 per troy ounce. This value was up 345% in nominal terms from 1980. In real terms, accounting for the impact of inflation, that gain falls to only 22%. In contrast, a dollar invested in the S&P 500 would have returned a 12,791% in nominal terms and 3,240% in real terms.

Will gold continue to rally?

There are reasons to think that gold will continue riding high. Goldman Sachs predicts the prices to climb to $3,100 by the end of 2025. Goldman Sachs bases its forecast on sustained central bank demand and geopolitical uncertainty. UBS has similarly adjusted its year-end forecast to $2,900, while Bank of America analysts have predicted $3,000 by year-end. Citigroup provides the broadest range, forecasting gold to trade between $2,700 and $3,200 over the next 12-18 months.

There remain concerns, however, about overvaluation. Many technical analysts point towards overbought conditions. If trade tensions ease, investors may turn away from their defensive positions. If inflation remains persistent, and interest rates are maintained higher for longer, the opportunity cost of holding a non-yielding asset like gold may dampen demand. Past examples serve as a reminder that even gold, despite its enduring allure, can lose its lustre through sharp corrections. In 1980 an all-time-high came and went. It was followed by a rapid decline of more than 50%, which carried on for the next 2 decades. In August 2011, gold reached another all-time high, following the 2008 crisis and fears of sovereign debt defaults in Europe. This rally peaked and swiftly unravelled. Those late to the trend were left holding positions that would take nearly a decade to recover. In July 2020, gold surged once more – this time driven by pandemic-related fears and unparalleled central bank interventions. The price pushed above $2,000. It wasn’t long before gold corrected.

Conclusion

Most investors welcome opportunities for portfolio diversification although, at current record highs, the hedging capabilities of gold may have become stretched. The geopolitical volatility that has characterised the first quarter of 2025 may, however, continue to drive gold prices higher in the short-term. The timeless questions remain – how enduring will this be? And, if a correction is due, when will it come and how seismic will it be? Whilst it’s impossible to predict the future with certainty, we would be looking to reduce gold allocations at these levels and take profits.

Recent market trends suggest that long positioning in gold has become crowded, indicating that the current gold price rally may be nearing its peak. With expectations of a ‘risk-off’ environment, much of the bullish positioning in gold could unwind. This shift could impact the outlook for gold in the near term, with market dynamics pointing toward a potential change in the current upward trend. As such, the risk reward favours a reduction in gold weightings.